Case Studies & Articles

Location: Sussex, UK

Value: 1,225,000

12th January 2023

UK Mortgage for Monaco Based Company Founder

Location: Monaco

Value: €16,000,000

We offer the following French mortgage solutions to international borrowers:

We cover all parts of the French mortgage market and have years of experience helping non-residents access the best rates.

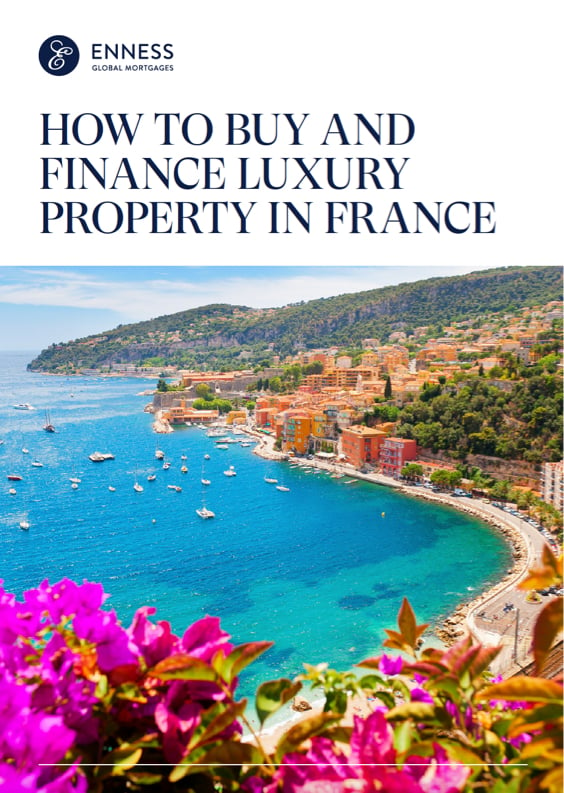

Request a CallabackIf you are purchasing a high-value property in France, you will most likely find yourself spoilt for choice. From a Parisian investment property to a second home on the Cote d'Azur or a holiday chalet in the Alps, France has something to offer every foreign property investor.

The Paris property market has always been resilient, and that's unlikely to change anytime soon, even for high-end properties.

The Parisian property market moves exceptionally quickly. There is both domestic and international buyer competition for the properties available, and liquidity is critical when securing real estate. Since Brexit, there has also been substantial British interest in Paris, with property purchases in the city fuelled by individuals who want to retain a euro asset as part of their post-Brexit strategy.

Generally speaking, the buoyancy of Paris' real estate means that French mortgages for non-residents are more readily available than in the other parts of France that also attract foreign investors. In addition, Parisian property – including luxury and high-end real estate – is typically always in demand. As a result, you will be able to generate income all year round if you wish to rent out your property to generate income.

While there are many options for financing a property purchase in Paris, you should note that French mortgages can be complex for international investors, especially if you are operating alone. French retail banks do offer mortgages to non-residents for Parisian property purchases. However, you will likely find that many of these will be very standardised packages that don't necessarily provide you with the most advantageous rates or terms as a foreign investor. Working with Enness will help you secure attractive mortgage rates and streamline the purchase process. You will also benefit from Enness' ability to structure your mortgage in a way that also considers taxation, mitigating exchange rate risk and the most advantageous legal structure for you.

France's Riviera has long been a magnet for foreign property investors and those looking for a second home or holiday bolthole in France. Situated on the Mediterranean coast of south-eastern France, the Côte d'Azur is home to some of the country’s most glamorous resorts.

Property prices on the Cote d'Azur's main resorts are relatively high. Domestic and international demand for property in the region continues to grow. As a result, you are likely to see a long-term and significant increase in property prices in this part of France.

As ever, time is of the essence if you want to buy a property on the Cote d'Azur. Ideally, you will want to have an in principle offer before you start the property purchasing process, or you work with a French mortgage broker like Enness, who can secure a French mortgage for non-residents very quickly. There can be competition for even the most expensive and high-end properties on the Cote d'Azur, and liquid buyers will find they hold a significant advantage over those who can't pit forward capital rapidly.

Lenders see properties on the Côte d'Azur as solid investments. As a result, many lenders are comfortable using them as security, given they are generally easy to sell and are likely to increase in value.

For this reason, Enness may be able to secure a mortgage for French property on the Côte d'Azur without you needing to pledge assets under management with your lender. You might find this appealing if you do not wish to initiate a private banking relationship with a lender.

On the other hand, if you are open to starting a new private banking relationship to help you get a more competitive French mortgage as a non-resident, Enness is likely to be able to negotiate loans on a 100% gross loan-to-value basis. To benefit from these kinds of terms, you will likely need to invest 20% of the mortgage amount with the lender.

It is safe to say that demand for prime luxury chalets in the French Alps is constant, and investments have proven to be secure and profitable for many property investors. Chalets can provide lucrative income streams if you wish to rent them out. You will generally find it easy to rent out property in the winter months, as people will flock to the region to ski. However, the French Alps can be popular in summer, too, with many tourists looking to rent property in warmer months.

The French Alps offer a unique environment but also deliver on both privacy and relaxation. Alpine property has always attracted huge demand, despite being in short supply. If you are looking to acquire property in the French Alps, expect significant competition as and when properties become available. Any delay in securing finance is likely to be the difference between a successful purchase and a prolonged wait.

Domestic French banks, international private banks and niche lenders offer mortgages in France for foreigners hoping to buy in the French Alps.

France's retail banks have a high appetite to offer mid-sized French mortgages for chalets in hotspots such as Chamonix and Morzine. Enness will often be able to negotiate these loans in such a way that lenders will offer high loan-to-value financing, as well as credit-only relationships. In short, you will not necessarily have to place assets under management with French retail lenders to buy in the region.

On the flip side of the coin, private banks also have an appetite for offering mortgages in France for foreigners wishing to buy in the Alps. However, if you want to borrow from a private bank to buy a property in the region, you will likely get the best rates and terms when you put assets under management with an institution. In essence, many private banks look to lend against Alpine properties in return for starting a professional relationship with you.

As a final point worth noting, the more liquid you are and the more diverse your assets, the fewer assets you are likely to need to have under management with your lender, regardless of where you are buying in France and the cost of your real estate transaction.

Generally speaking, it's advisable to think about property financing early, especially when buying in France. Getting the best French mortgages for non-residents is rarely as simple as popping into a local bank and coming out with a superb deal. The best rates and terms are generally offered by key players working for a few select lenders – these might be domestic or international institutions. Each lender will have a different appetite for different types of borrowers, which includes the type of property you are buying, the cost of the real estate at the centre of the transaction and the region where you want to purchase. Of course, your financial situation, the assets you bring to the table and your global wealth will also hold sway.

If you haven't already secured an in principle offer for property finance, you may also struggle to find lenders who can meet the speed of your transaction – the more expensive your property, the harder this will become if you are working alone. Finding lenders who have an appetite for high-value property deals through your own contacts or parties you can approach directly can also be a challenge. Enness have access to more than 500 lenders. The firm is also independent, which means your broker is free to seek out the best deal for you from anyone in the market.

When it comes to the details of how to get a mortgage in France, Enness will work closely with you to understand your requirements for a French mortgage. Practically speaking, this will include:

The French mortgage market is competitive, and lots of different elements can be negotiated, depending on where you are prepared to be flexible or grant concessions to lenders in return for a better deal or more advantageous rates. It's very typical to have ''non-negotiables,'' too. These are often just as important as the terms you are looking for, and Enness will be able to negotiate a mortgage for you that takes of your wishes into consideration. With a firm understanding of what you want, Enness will look at what to present and emphasise to lenders to present your case as powerfully as possible.

Working with a partner that knows exactly how to get a mortgage in France will help you secure property finance faster and with less stress. Brokering international mortgages since 2007, Enness knows exactly who to approach and which lenders will offer the best French mortgages for non-residents that meet your criteria. In addition, your broker will know if it's best to negotiate with domestic or international lenders. They will also build you a mortgage vehicle that's as tax efficient as possible.

Regardless of your situation and background, Enness will be able to help you secure a competitive mortgage. For example, if you want to buy property in France, but you have a complex background that may dampen the appetite of French retail banks, Enness knows the lenders that will grant you a mortgage for a French property.

Enness knows which lenders will lend to you and offer you competitive property financing in France, even if you:

Enness will be able to help you secure a mortgage regardless of your nationality, residence, or background. French property remains highly attractive for foreign investors, and Enness has the capability, skill, lender access and language capabilities to secure French property finance for any high-net-worth client or family.

Whether you are an international property investor or wish to buy a second home or holiday property in France, getting a mortgage in France can make a lot of sense. French chalets, apartments, and houses can easily run to millions of euros, especially in Paris and other popular regions like the Cote d'Azur and the Alps. As a result, mortgages are commonplace for France's foreign property investors and second homeowners. Principally, they use mortgages to retain liquidity as they can avoid putting down significant cash or liquidating assets to buy a high-value property outright.

French mortgages for non-residents can also make a lot of sense from a tax planning perspective. Depending on your personal situation, nationality and residence, mortgages can effectively be used to streamline the cost of your property investment.

You should also know that if you want a mortgage for French property, that doesn't necessarily mean you need to be looking for a mortgage from a French bank or lender. In many cases, international private banks and other lenders will offer more advantageous loans than France’s domestic lenders. France's buoyant property market and stable real estate prices has meant that there has been an influx of international lenders who are interested in offering competitive mortgages in France for foreigners over the past few years.

Broadly speaking, mainstream French mortgage companies enforce very strict debt serving ratios, and these firms focus almost exclusively on your liquidity and income. Therefore, borrowers who can put down very significant deposits, who already have French assets they can use as security and who can prove they are very liquid can fare better with these lenders. On the other hand, foreign income, significant expenses and lots of foreign assets (even if they are substantial and liquid) can make it harder to get a mortgage for French property from this specific group of lenders.

As a result of the challenges of working with domestic retail banks, international and private banking institutions quickly moved to provide mortgages for non-residents. These institutions recognised that taking a very local view of assets and liquidity prevented foreign property investors from getting a French mortgage, even if they had very strong financial backgrounds and significant wealth and assets. As a result, international and private banks will understand the need to assess your worldwide income and overall wealth to calculate eligibility for property finance. Many also offer the option to lock in relatively low interest rates for between five and ten years.

If you are a UK resident and wish to secure a mortgage on French property, planning will be critical to your success. While there is nothing to stop you from getting a mortgage in France, the process is more complex than when the UK was part of the EU bloc, and French lenders can be a little more guarded or take longer to make decisions. Also, note that as a non-EU citizen, you may be liable to pay more for a French mortgage than you would have as an EU citizen.

The rates and terms of French mortgages for UK residents can vary significantly from lender to lender. France's domestic lenders will look in close detail at your income and the affordability of your mortgage in comparison. They are also likely to have other criteria you will need to meet as a UK resident. What you want to do with your property will also play a part – some lenders will be more open to letting you borrow if you will rent out your French property and will derive a source of income from it. On the other hand, they may be less eager to lend if you are purchasing a holiday home or second residence exclusively for your personal use.

For UK residents who are high-net-worth borrowers, the story is likely to be a little different. In this case, obtaining a mortgage may well be easier. Private banks remain willing to lend, especially to the UK resident high-net-worth individuals that will consider placing assets under management with them. Private banks can sometimes be less rigid in their lending criteria for UK residents – where income is especially important for France's retail lenders, private banks are generally more than happy to assess you on the basis of your global assets, net worth and other factors that can positively influence your mortgage rate.

Overall, Enness will source and negotiate attractive property finance for UK residents. Especially as a UK resident looking to get a mortgage in France, you will reap the rewards of working with a French mortgage broker that knows which lenders to approach and how to secure a mortgage for you quickly and with a minimum of stress.

Interest rates in France are incredibly low, thanks to the prevailing EURIBOR rates. As a result, lending terms can be very attractive.

Enness will build a mortgage vehicle for you from scratch so that you benefit from property financing that meets all your needs and is structured in a way that's cost-efficient considering your circumstances. Generally speaking, this means there are two approaches when it comes to French mortgages for non-residents:

Interest-only mortgages are available for French non-resident property investors. Long term fixed-rate mortgages might also be an option for you.

If you are seeking out lenders alone, however, the process for negotiating and securing a French mortgage can be bureaucratic and will require significant amounts of your time. Enness has considerable experience to counter these problems and will be able to save you time, speed up the process and secure the best rates for you.

French expat mortgages are among some of the most complicated property financing deals. If you are an expat, you will need to consider how you structure finance carefully. French mortgage companies traditionally lend funds up to 85% for properties with a value up to €5 million for expats.

To secure French mortgages as an expat, you will likely need to reveal your worldwide income and expenditure. Typically, the debt serving ratio cannot exceed 35% of your income, which can be problematic if you have complex finances.

For luxury and ultra-prime property, one of the best routes to getting a mortgage in France is to borrow from a private bank. Private banks have a different outlook from their commercial counterparts and tend to be more flexible with mortgage deal requirements.

Typically, you will find that to get a mortgage for French property from a private bank, the bank will require an asset pledge if the value of your French mortgage is at €1 million or above. The amount you will be required to put forward will vary from bank to bank but tends to sit between 20% and 50% of the outstanding mortgage with equity release considered in the right environment. Enness will advise you on the type of assets you might want to use as collateral and when you should request equity release along the way.

If you want to develop a French property, Enness can help you source and negotiate development funding. Enness has contacts in international financial markets who also facilitate development funding for up to 100% of the project cost. Development finance can cover practical work on French property, including:

Engineering

Architecture

Development finance can also cover Notary fees.

You’ll want to structure French development finance carefully to ensure you benefit from the most advantageous rates and terms. It is possible to mitigate French wealth tax if the transaction is structured to involve the transfer of capital or assets into an asset management arrangement, for example. This can be as low as 20% of the development finance with a portion of assets under management allowed from loan capital. Only careful structuring to capture the regulations that allow for tax efficiency will open up these opportunities for you, so ensure you don't miss the possibilities to do so.

Enness can negotiate mortgages in any currency, and your broker will structure property finance in the currency that is best for you or that gets you the best rates. In some cases, this will mean a euro mortgage may well be the best option for you. French mortgages can be fixed-rate, variable-rate, EURIBOR tracker, capped or a hybrid structure to add a degree of stability. Interest rates can currently be fixed at around 1.5% due to the historic low level of base rates across Europe. Enness will build mortgages around your situation to minimise finance costs and enhance your long-term returns.

When it comes to getting a mortgage in France, it's vital that you don't make the (common) mistake of assuming France has a like-for-like scenario with your home country or place of residence.

Taxation and regulations can vary from country to country, and France's legal and fiscal system is one of the more complex to navigate. As a result, you will want to ensure your property finance is well structured so that you benefit from the best – and most efficient – deal. Enness will advise you on all aspects of your finance deal and will build a financing package that considers everything from taxation to foreign exchange risk, optimised legal structuring and insurance. When it comes to French mortgages for non-residents, there's a lot to choose from with ''plain vanilla'' property finance, refinancing, development finance, equity release and bridging finance all readily available. Enness also have a track record completing on an array of specialist projects such as leaseback arrangements and Vente en l’état futur d'achèvement VEFA) contracts for off-plan French property.

Enness' experience and contacts are spread right across the field of finance. Therefore, you can expect your broker to bring you the best deal structure with the lowest financing costs. Enness will also help you arrange property finance that mitigates legal costs (up to 7.5%) and the French wealth tax (1.5%) by structuring your mortgage finance in the most efficient manner. Your broker will also be able to source preferential rates and terms that are not readily available to others.

Enness has significant experience assisting high-net-worth non-residents in securing competitive and advantageous mortgages in France.

Contact Enness to have a no-obligation chat about your plans for purchasing property in France and explore how Enness can help you structure and streamline French property finance.

Get In Touch NowFrance is one of the most popular property markets for foreign nationals: we are all aware of the chic appeal of Paris, the enduring allure of the Riviera in the summer or the freshness of the mountains in winter.

However, buying a property in France, especially as a foreign national or non-resident is particularly difficult. France’s legal and financial systems are unique. Culture and customs are often a learning curve.

Here at Enness, we are lucky to work with many of the leading experts in the French market: real estate agents, search agents, notaries, and developers. Together, we cover every aspect of the French property market and the buying process.

Location: Sussex, UK

Value: 1,225,000

Location: Monaco

Value: €16,000,000